Thrift Savings Plan (TSP) for Air Force Members

The Air Force gives you free money every month you’re on active duty, and most junior airmen never collect all of it. The Thrift Savings Plan is a retirement account that works like a civilian 401(k), but the government contributes to yours on top of whatever you put in. Miss the rules and you lose that match permanently.

This guide covers everything you need to know: how the matching works, how much you can contribute, which funds to use, and the one mistake that kills your match before December.

What the TSP Is and How It Fits the BRS

The Thrift Savings Plan is a tax-advantaged retirement account run by the federal government. For Air Force members who entered service on or after January 1, 2018, it is the central piece of the Blended Retirement System (BRS).

The BRS replaced the old legacy pension as the default system. Under it, you still get a monthly pension at 20 years, but the multiplier is lower than the old system. The TSP match compensates for that gap, but only if you use it.

There are three ways money flows into your TSP under BRS:

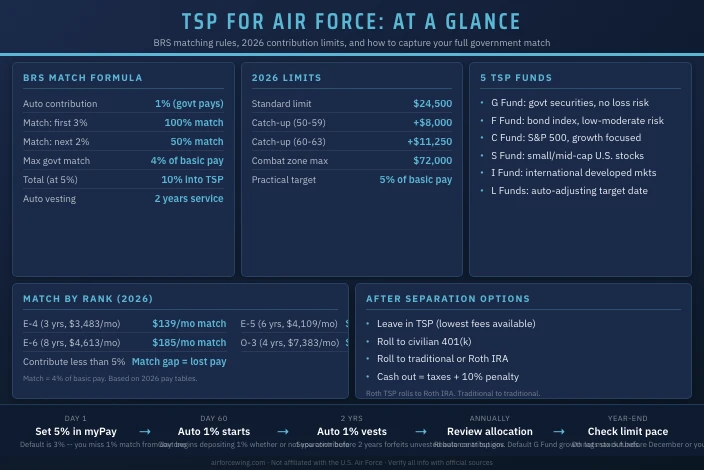

- Automatic 1% contribution: The government deposits 1% of your basic pay into your TSP starting 60 days after you enter service. You get this whether or not you contribute anything yourself. It vests after two years of service.

- Matching contributions: For every dollar you contribute, the government matches dollar-for-dollar on the first 3% of basic pay, then 50 cents per dollar on the next 2%. Contribute 5% and the government adds 4%.

- Your own contributions: Whatever you elect to contribute beyond 5%, up to the IRS annual limit.

The combined maximum government contribution is 5% of your basic pay (1% automatic plus 4% in matching). That’s money you earned. Not collecting it by contributing at least 5% yourself is a pay cut.

BRS Matching Math: What You Actually Get

The matching schedule is straightforward once you see it in a table.

| Your contribution | Government match | Total going in |

|---|---|---|

| 0% | 1% auto only | 1% |

| 1% | 1% auto + 1% match | 3% |

| 3% | 1% auto + 3% match | 7% |

| 5% | 1% auto + 4% match | 10% |

| 6%+ | 1% auto + 4% match | 7%+ (match capped) |

Contributing 5% of basic pay gets you the maximum 10% total going into your account every month. An E-4 with three years of service earns about $3,483/month in basic pay. At 5%, that airman puts in $174/month and the government adds $139 in matching plus the $35 automatic contribution. That totals $348 deposited per month, half of it free.

At SSgt (E-5) with six years of service, basic pay is $4,109/month. The same math produces $411/month going into TSP from a $206 personal contribution.

Contribution Limits for 2026

The IRS sets annual limits on how much you can put into tax-advantaged accounts. For TSP in 2026:

- Standard limit: $24,500 (up from $23,500 in 2025)

- Catch-up for age 50-59 and 64+: additional $8,000 allowed

- Catch-up for ages 60-63: additional $11,250 allowed (SECURE 2.0 enhanced limit)

- Combat zone limit: $72,000 annually, including tax-exempt pay

Most junior enlisted members will never hit $24,500. An E-3 earning $3,015/month would need to save nearly 68% of gross pay to reach it. The practical target is 5% to capture the full match, then increase contributions as pay rises with promotions.

One critical rule: do not max out your contributions before December. The matching happens each pay period. If your contributions run out in October, you lose two months of government matching with no way to recover it.

Traditional vs. Roth TSP

You can contribute to a traditional TSP (pre-tax dollars, taxed at withdrawal) or a Roth TSP (after-tax dollars, tax-free withdrawals in retirement). The government match always goes into the traditional side regardless of your election.

For most junior airmen, Roth tends to make more sense. You’re likely in a lower tax bracket now than you will be later in your career. Paying taxes at today’s lower rate and never paying taxes on the growth or withdrawals is usually the better deal.

A few scenarios where traditional TSP makes sense:

- You’re a senior NCO or officer at a high tax bracket now

- You expect your retirement income to be modest

- You’re deployed to a combat zone and your pay is already tax-exempt (contributions made from tax-exempt combat-zone pay are treated as Roth)

There’s no rule forcing you to pick one. You can split contributions between both in any percentage.

The Five TSP Funds

The TSP offers five individual funds. Each tracks a specific market index or government security.

| Fund | What it tracks | Risk level |

|---|---|---|

| G Fund | Special U.S. Treasury securities (guaranteed no loss) | Lowest |

| F Fund | Bloomberg U.S. Aggregate Bond Index | Low-moderate |

| C Fund | S&P 500 (large U.S. companies) | Moderate-high |

| S Fund | Dow Jones U.S. Completion TSM (small/mid-cap U.S. companies) | High |

| I Fund | MSCI EAFE (international developed markets) | High |

The TSP also offers Lifecycle (L) Funds, which are pre-mixed allocations that automatically shift toward more conservative holdings as your target retirement year approaches. If you don’t want to manage your own allocation, the L Fund closest to your planned retirement year is a reasonable default.

The G Fund is where contributions land by default if you never change your allocation. The G Fund doesn’t lose value, but long-term returns lag behind stock funds significantly. A 25-year-old whose TSP sits in the G Fund for 20 years is leaving substantial growth on the table.

A common starting point for younger airmen is heavy C Fund exposure, often 80% or more, with smaller allocations to S and I Funds for diversification. A financial counselor at your installation’s Airman and Family Readiness Center can help you build an allocation that fits your situation. This article does not constitute financial advice.

When the Match Vests

Vesting means you own the money. Your own contributions vest immediately. The automatic 1% government contribution vests after two years of service.

The matching contributions vest based on when they are earned relative to your two-year mark. Once you hit two years of service, all matching contributions vest as they come in.

If you separate before hitting two years, you forfeit the automatic 1% contributions and any unvested matching. Your own contributions are always yours.

Managing Your TSP Account

Your TSP account is separate from myPay. Log in at tsp.gov to:

- Change contribution amounts and types (traditional vs. Roth)

- Adjust your fund allocations

- Set up automatic rebalancing

- Designate a beneficiary

Changes made in myPay affect contribution percentages deducted from your paycheck. Changes made at tsp.gov affect where the money goes once it’s in your account. You need both sites.

Set your contribution election on day one. The default enrollment that happens under BRS puts you at 3%, which means you’re leaving 1% of match on the table from day one. Log into myPay and set it to 5%.

TSP After Separation

When you leave the Air Force, you have four main options for your TSP balance:

- Leave it in TSP: Often the best choice. TSP has some of the lowest expense ratios of any retirement account in the country.

- Roll it into a civilian employer’s 401(k): Works well if your new employer’s plan has good fund options and low fees.

- Roll it into an IRA: Gives you more investment choices. Roth TSP rolls to Roth IRA; traditional TSP rolls to traditional IRA.

- Cash it out: Triggers income taxes plus a 10% early withdrawal penalty if you’re under 59½. Almost always the worst option.

Reserve component service members should know the TSP rules work somewhat differently. Contributions and matching still apply during periods of active duty orders, but the timeline and vesting rules vary. Check with your unit’s financial readiness officer.

Learn more about Air Force pay, allowances, and benefits to see how the TSP fits the full compensation picture.

Browse Air Force enlisted careers to see how pay progresses across different AFSC career fields. You may also find Air Force pay and benefits overview helpful for context on basic pay figures and the broader BRS framework.

This site is not affiliated with the U.S. Air Force or any government agency. Verify all information with official Air Force sources before making enlistment or career decisions.