Air Force Healthcare: TRICARE Explained for New Airmen

Civilian health insurance costs the average American worker roughly $8,000 a year in premiums alone. Active duty Airmen pay zero. No enrollment fee, no deductible, no copay at the doctor’s office, and the coverage extends to your entire family.

That’s not a benefit buried in the fine print. It’s one of the most concrete financial advantages of Air Force service, and it starts on day one of Basic Military Training. This guide explains exactly how the system works, what it covers, and what changes when you move to the Reserve.

How TRICARE Works for Active Duty Airmen

The military healthcare system is called TRICARE. Active duty Airmen are automatically enrolled in TRICARE Prime, a managed care plan that works similarly to a civilian HMO.

You don’t have to apply or choose a plan. The enrollment happens automatically when you enter service. A primary care manager (PCM) handles your routine care and refers you to specialists when needed.

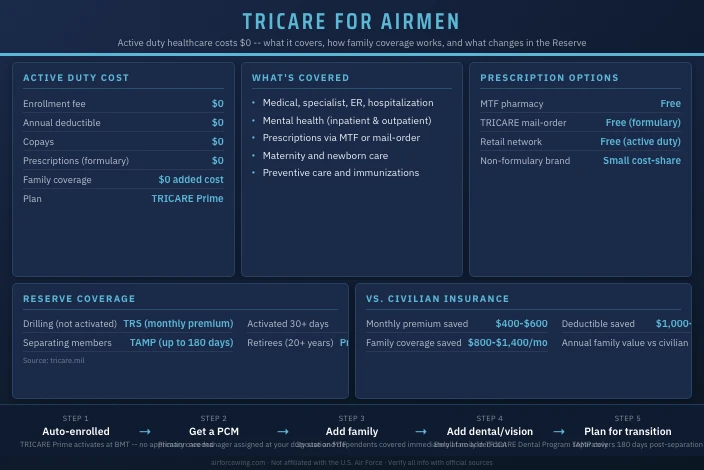

The cost structure for active duty members is straightforward:

| Cost Component | Active Duty Member |

|---|---|

| Enrollment fee | $0 |

| Annual deductible | $0 |

| Copays | $0 |

| Prescription (formulary) | $0 |

| Specialist visit (with referral) | $0 |

There is no annual cap on covered services for active duty members. If you need surgery, hospitalization, or ongoing treatment, TRICARE covers it without cost-sharing.

What TRICARE Prime Covers

The scope of coverage is broad. TRICARE Prime covers:

- Medical care: Primary care, specialist visits, emergency treatment, hospitalization

- Mental health: Inpatient and outpatient behavioral health services

- Prescriptions: Most formulary drugs at zero cost through a military treatment facility pharmacy or the TRICARE mail-order program

- Preventive care: Annual physicals, immunizations, cancer screenings

- Maternity care: Prenatal visits, labor, delivery, and postpartum care

- Physical therapy and rehabilitation: With a referral from your PCM

One thing new Airmen sometimes miss: using civilian providers outside the military treatment facility (MTF) network requires a referral and prior authorization. Going out of network without one can create out-of-pocket costs. Always start with your PCM.

Family Coverage Under TRICARE

Your spouse and dependent children are covered the moment you enter active duty service. They are automatically eligible as TRICARE Prime beneficiaries.

Family members receive the same zero-cost-sharing structure for most care. The details:

- Spouses and children under 23 (enrolled in school) are eligible dependents

- Coverage begins immediately, no waiting period

- Family members also have a PCM assigned and follow the same referral process

- Newborns are covered from birth

One difference: civilian emergency care for family members may carry a small cost-share if no MTF is accessible. Confirm your specific plan details at tricare.mil when you arrive at your first duty station.

Dental and Vision

TRICARE Prime does not include full dental or vision coverage as a default benefit for family members. The coverage structure is:

Dental:

- Active duty members receive dental care free at the MTF

- Family members enroll separately in the TRICARE Dental Program (TDP), which carries a low monthly premium and covers preventive and restorative care

- Orthodontic coverage is available under TDP with cost-sharing

Vision:

- Active duty members receive routine eye exams and corrective lenses through the MTF

- Family members use the TRICARE Vision benefit for one annual exam covered under Prime, but eyeglasses and contacts require out-of-pocket spending or a separate vision plan

If your family uses a lot of dental or vision services, it’s worth pricing out the TDP and any supplemental vision plan early in your service.

Prescriptions: Three Ways to Fill Them

TRICARE offers three options for getting prescriptions filled, each at a different cost tier for active duty members:

- MTF Pharmacy: Free. This is always the first option to check. On-base pharmacies carry the most commonly prescribed drugs at no cost to active duty members.

- TRICARE Pharmacy Home Delivery (Express Scripts): Free for most formulary drugs. Good for maintenance medications like blood pressure or allergy prescriptions.

- Retail Network Pharmacy: Free for active duty members at in-network civilian pharmacies. Useful when you’re off base and need a prescription filled quickly.

Non-formulary drugs (brand-name when a generic exists) may carry a small cost even for active duty members. Ask your prescriber whether a generic equivalent is available.

TRICARE for Reserve and Guard Members

Reserve and Air National Guard members are not automatically enrolled in TRICARE. Coverage eligibility depends on activation status.

| Status | Coverage Available |

|---|---|

| Drilling reservist (not activated) | TRICARE Reserve Select (monthly premium) |

| Activated for federal service (30+ days) | TRICARE Prime (same as active duty, no cost) |

| Transitioning off active duty | TRICARE Transitional Assistance (180 days, premium) |

TRICARE Reserve Select (TRS) is the standard option for drilling reservists. It works like TRICARE Prime but requires a monthly premium. Rates vary and are updated annually, check tricare.mil for current premiums.

Once a Reservist activates for more than 30 consecutive days, they shift to the same zero-cost TRICARE Prime coverage active duty members receive. That coverage ends when they return to drill-only status.

When Coverage Ends

Active duty TRICARE coverage doesn’t follow you the moment you separate. The timeline:

- Active duty separation: Coverage ends the day after your separation date

- Retirement (20+ years): You transition to TRICARE Prime or TRICARE Select as a retiree, with cost-sharing requirements

- Transitional coverage: Separating members can purchase Transitional Assistance Management Program (TAMP) coverage for up to 180 days after separation

The transition window matters. If you’re separating without a civilian job lined up, budget for either TAMP premiums or a marketplace plan. Many Airmen underestimate the gap.

Comparing TRICARE to Civilian Insurance

To put the value in concrete terms, here’s how TRICARE Prime compares to a typical employer-sponsored plan:

| Feature | TRICARE Prime (Active Duty) | Typical Civilian Plan |

|---|---|---|

| Monthly premium | $0 | $400-$600 (employee share) |

| Annual deductible | $0 | $1,000-$3,000 |

| Copay per visit | $0 | $20-$60 |

| Out-of-pocket max | $0 | $5,000-$10,000 |

| Prescription (generic) | $0 | $10-$30 |

| Family coverage added cost | $0 | $800-$1,400/month additional |

The annual value of TRICARE Prime for a family of four, compared to a mid-range civilian employer plan, often exceeds $20,000 when you account for premiums, deductibles, and copays that simply don’t apply.

For a full breakdown of all Air Force compensation components including pay tables and housing allowances, see the complete guide to Air Force pay and benefits.

Medical AFSC careers are a natural fit for Airmen interested in healthcare at the professional level. The Air Force medical career group covers enlisted roles ranging from aerospace medical technicians to surgical service technicians, each with different training pipelines and civilian credentialing pathways.

The Air Force benefits guides cover healthcare alongside housing allowances, education programs, and retirement, useful if you want the full financial picture in one place.

This site is not affiliated with the U.S. Air Force or any government agency. Verify all information with official Air Force sources before making enlistment or career decisions.