Air Force Retirement: BRS Pension Calculator and Timeline

Retire after 20 years and the Air Force pays you a monthly pension for the rest of your life. That single fact makes military retirement one of the most valuable benefits in any career. But the system changed in 2018, and many Airmen still don’t fully understand how the Blended Retirement System works or what they’ll actually receive.

This post covers the pension formula, what the TSP matching means in real dollars, and the key decisions at each stage of a 20-year career.

How the BRS Pension Works

The Air Force Blended Retirement System pays a pension based on one formula.

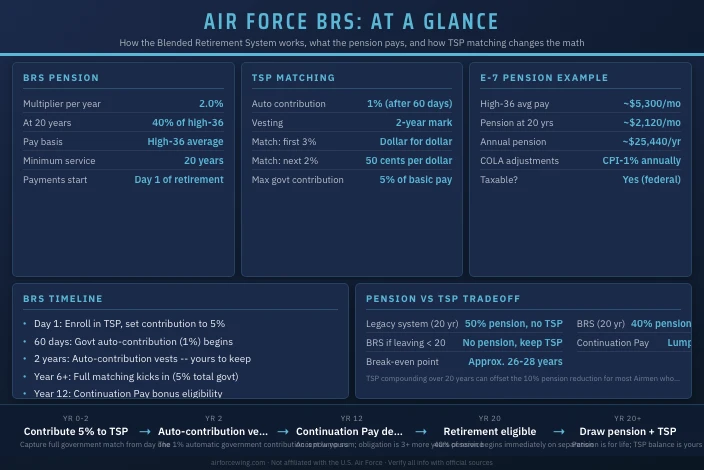

Pension = years of service x 2% x high-36 average basic pay

The high-36 is the average of your highest 36 months of basic pay. For most Airmen on a standard career track, that’s the final three years before retirement when pay is at its peak.

At exactly 20 years, the multiplier works out to this:

20 years x 2% = 40% of your high-36 average

That 40% figure is permanent. It starts the day you separate and continues for life, with annual cost-of-living adjustments tied to the Consumer Price Index minus 1%. Payments are taxable at the federal level.

Before BRS, the Legacy High-3 system paid 50% at 20 years with no TSP matching. The BRS trade-off is a lower pension multiplier in exchange for government contributions to your TSP retirement account starting early in your career.

What the Pension Actually Pays

Pension size depends on your rank and years of service at retirement. The table below shows realistic estimates based on the 2026 pay tables, assuming a Airman retires at exactly 20 years.

| Rank at Retirement | High-36 Avg Pay (est.) | Monthly Pension | Annual Pension |

|---|---|---|---|

| E-6 Technical Sergeant (TSgt) | ~$4,900/mo | ~$1,960/mo | ~$23,520/yr |

| E-7 Master Sergeant (MSgt) | ~$5,300/mo | ~$2,120/mo | ~$25,440/yr |

| E-8 Senior Master Sergeant (SMSgt) | ~$6,600/mo | ~$2,640/mo | ~$31,680/yr |

| O-4 Major (Maj) | ~$9,800/mo | ~$3,920/mo | ~$47,040/yr |

| O-5 Lieutenant Colonel (Lt Col) | ~$11,500/mo | ~$4,600/mo | ~$55,200/yr |

These are estimates based on typical promotion timelines. Your actual high-36 depends on when you were promoted and how long you held each pay step. The DFAS military retirement calculator lets you plug in your own service record for a precise figure.

Each year past 20 adds another 2.5% to the multiplier. Serving 24 years brings the pension to 48% of high-36. At 30 years, it reaches 75%, which is the BRS maximum.

TSP Matching: The Other Half of the Equation

The pension is one part of BRS. The TSP matching is where the system changes the math for Airmen who don’t make it to 20 years.

Government TSP contributions work in three layers:

- Automatic 1%: The government deposits 1% of your basic pay into your TSP account starting 60 days after your first day of service. You don’t have to contribute anything to receive this.

- Matching your contributions: Once you contribute to TSP yourself, the government matches 100% of your first 3% and 50% of the next 2%. That caps the match at 4%.

- Total government contribution: Add the automatic 1% to the 4% match and the government puts in 5% of basic pay if you contribute at least 5%.

The automatic 1% vests at the 2-year mark. Leave before then and you forfeit it. Stay past year two and the entire balance is yours to keep even if you never reach 20 years.

To capture the full match, contribute at least 5% of basic pay to TSP starting with your first paycheck.

The Continuation Pay Decision

BRS includes a one-time lump sum called Continuation Pay, offered somewhere between years 8 and 12. Both officers and enlisted Airmen receive it, though the payout multipliers differ by service need and career field.

The payment comes in exchange for a minimum 3-year service obligation. Before accepting, consider three things:

- Continuation Pay is taxable in the year you receive it. A large lump sum can push you into a higher bracket if you haven’t planned for it.

- The service obligation is firm. Circumstances change; the contract doesn’t.

- Depositing Continuation Pay into TSP (up to the annual IRS contribution limit) is one of the most effective ways to close the gap between BRS and what the old Legacy system would have paid.

BRS vs Legacy: The Break-Even Math

The enrollment window for switching between systems closed in 2019, but the comparison explains why the TSP piece matters. Airmen who entered service on or after January 1, 2018 are automatically on BRS with no choice.

| Factor | Legacy High-3 | Blended Retirement System |

|---|---|---|

| Pension at 20 years | 50% of high-36 | 40% of high-36 |

| Government TSP match | None | Up to 5% of basic pay |

| Benefit if leaving before 20 | Nothing | TSP balance you keep |

| Continuation Pay | No | Yes (years 8-12) |

The break-even point, where cumulative BRS pension value catches up to Legacy, falls around 26 to 28 years of pension payments after retirement. Beyond that, a Legacy retiree pulls slightly ahead in total pension dollars. Before it, an Airman who maximized TSP contributions under BRS is often ahead on total wealth.

The 10% pension reduction in BRS looks larger than it is. Compound growth on 20 years of matched TSP contributions closes most of the gap for Airmen who contribute consistently.

Building Toward 20: The Year-by-Year Timeline

Retirement planning starts at enlistment, not year 18. Each career window has a specific financial action that affects the final outcome.

Reserve and Guard Retirement

Reserve and Air National Guard Airmen earn retirement through a points-based system rather than continuous years of active duty. Each day of active service, drill weekend, and annual training period earns points. A minimum of 20 qualifying years (at least 50 points per year) is required to become eligible.

The critical difference from active duty retirement: Reserve benefits don’t begin until age 60, not at separation. That age can be reduced by 3 months for every 90 days of qualifying active duty served after January 28, 2008, with a floor of age 50.

The formula uses total lifetime points divided by 360 as the years-of-service equivalent, then applies the same 2% multiplier against the retired pay base. A reservist with 2,900 lifetime points would calculate 2,900 / 360 = ~8.06 equivalent years, yielding about 16% of their retired pay base.

Reserve component retirement math is worth tracking annually once you cross 15 qualifying years. The Military OneSource BRS guide covers both active and reserve components in detail.

This site is not affiliated with the U.S. Air Force or any government agency. Verify all information with official Air Force sources before making enlistment or career decisions.

For a full breakdown of Air Force compensation including housing allowance, TRICARE, and GI Bill, see the Air Force pay and benefits guide. You can also browse the complete Air Force benefits overview and explore enlisted career paths to see how AFSC choice affects long-term pay and retirement projections.